Veggie burgers and market panic: what’s really going on?

While headlines scream “Vegan burgers are losing the US culture war over meat” or “The fake meat fad is over” (Quartz), it’s worth pausing for a moment. Are we really witnessing the death of the veggie burger, or the natural evolution of a market growing up?

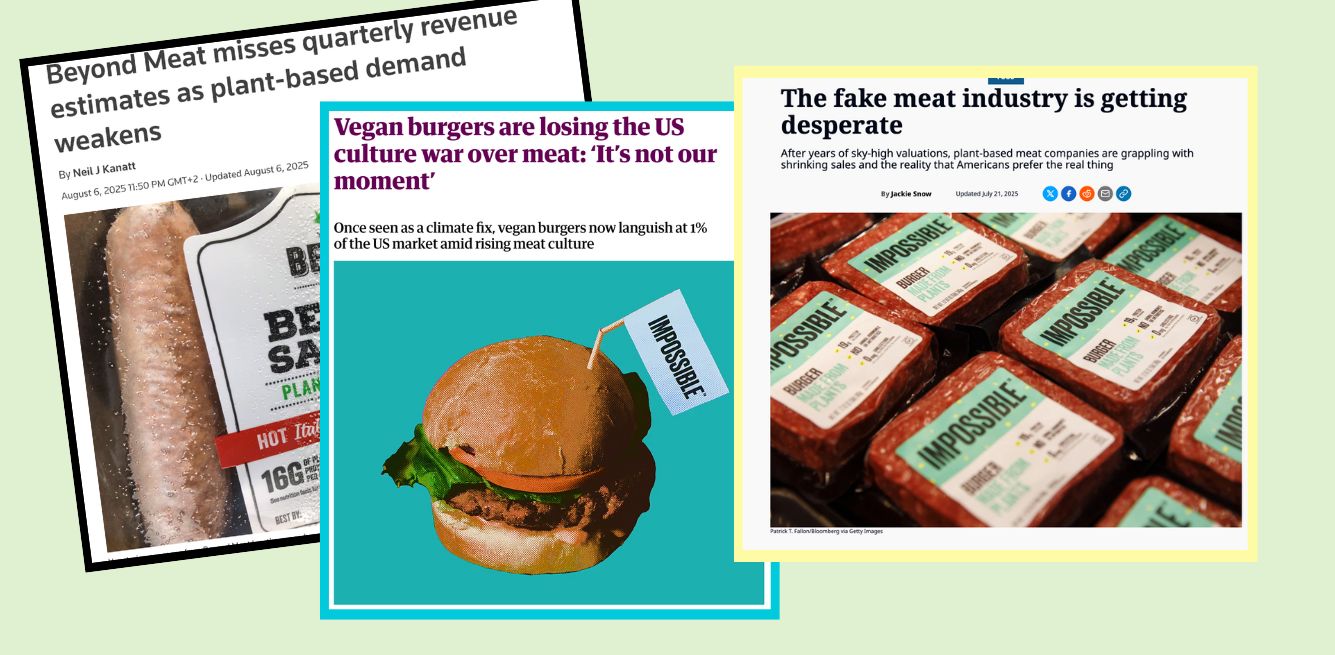

The numbers coming out of the United States—sales down 17%, Beyond Meat’s stock value plummeting, Impossible Foods announcing layoffs—paint a clear but narrow picture. They describe an American moment for the vegan industry, not its global fate.

When food becomes politics

In the US, the collapse of the veggie burger is, above all, a cultural story. Meat has turned into a political symbol in the Trump era, and vegan alternatives have become collateral damage in a wider identity war that has little to do with taste or nutrition. When the Secretary of Health toasts with raw milk at the White House and conservative influencers turn the “carnivore diet” into a patriotic badge, it’s obvious the debate has moved from the plate to the battlefield of belonging.

Food choices have become statements. Eating a veggie burger no longer just means trying something new. It means taking sides. And in a country where the myth of the cowboy collides with the rhetoric of “Make America Great Again,” the outcome was predictable.

The real strategic mistake of US companies like Beyond Meat and Impossible Foods was to underestimate this dynamic. They built their brands around rational arguments—sustainability, health, innovation—in an environment that had become profoundly irrational. The result was a fatal disconnect between message and audience.

Europe’s quiet resilience

Across the Atlantic, the picture looks entirely different, and the numbers speak for themselves. Europe isn’t fighting a culture war over what’s on the plate. Here, the transition is economic, not ideological.

France: +8.8% growth in plant-based sales in 2024.

Germany: +7.1% in volumes.

Italy: 15 million households buying plant-based products, a 59.3% penetration rate and a 10% increase in purchase frequency (YouGov Shopper).

These data aren’t signs of a passing trend. They mark the consolidation of a mature market. In Europe, plant-based eating isn’t an identity threat; it’s an expansion of choice.

Italy’s growth is especially telling: it proves that flexitarianism—a pragmatic approach that integrates rather than replaces—works when it’s free from ideological barriers. 38% of households buying plant-based deli products aren’t militant vegans. They’re ordinary consumers who have simply normalised these foods as part of their everyday routine.

The price factor

A key reason behind the transatlantic divergence is pricing. In the US, veggie burgers have stayed stubbornly premium, often twice the cost of conventional meat. In Europe, supermarket private labels have democratised access, making vegan options affordable and scalable.

That’s not a technicality, it’s a strategic turning point. The vegan sector can either remain a niche for the ideologically motivated or become a mainstream alternative. European data suggest the latter path is far more sustainable.

According to Coop’s 2025 Report, beef sales are slightly down (-0.9%), while plant-based deli foods are up a striking 20.9%. It’s not a radical replacement but a slow rebalancing of the grocery basket—driven by price as much as by environmental awareness.

Beyond imitation

The obsession with “meat-like” burgers risks overshadowing the real story. The vegan sector is evolving beyond mimicry. It’s shifting from imitation to diversification: protein alternatives, dairy-free innovations, ready-made plant-based meals.

Consumers no longer crave the fake. They’re after the alternative. This is a cultural shift as much as a commercial one, moving plant-based food from the realm of ideology into the everyday logic of convenience and variety.

Even the pioneers are adapting. Beyond Meat has announced plans to drop “Meat” from its name, rebranding itself as a “protein company.” That’s not a surrender, it’s a recalibration to match the market’s new phase.

A reality check

The financial euphoria of 2018-2021, with billion-dollar valuations for companies still years away from profit, was never going to last. The current slowdown isn’t the end of plant-based—it’s its normalisation.

This landing phase is healthy. It forces companies to focus on profitability, efficiency, and product quality rather than lofty promises. It grounds the industry in reality: price, taste, availability, and communication.

The survivors of this consolidation won’t be those that shouted the loudest, but those that built solid, sustainable business models.

Transition, not revolution

The vegan sector isn’t collapsing, it’s transitioning. The revolutionary hype is giving way to the steady management of an established market. Every innovative industry goes through this maturing phase.

European and Italian data show that success lies in pragmatism: quality, accessibility, and inclusion—not ideology. The future of plant-based products won’t be decided by flashy headlines or stock market swings, but by their ability to become a normal, affordable part of everyday diets.

The American experience, marked by inflated expectations, high prices, and culture wars, offers Europe a valuable lesson in what to avoid. The European path—gradual growth, product diversity, mainstream integration—shows what sustainable evolution really looks like.

This isn’t the end of a story. It’s the beginning of a new reality.

The VEGANOK Osservatorio: anatomy of two development models

At VEGANOK Osservatorio, our reading of the data suggests that the so-called “collapse” of veggie burgers actually reveals two radically different development models.

The American model bet everything on technological disruption with hyper-realistic products, billion-dollar investments, and promises to replace meat entirely. That approach created unsustainable expectations and premium prices that confined demand to affluent urban early adopters. Once political polarisation turned plant-based burgers into a culture-war symbol, the model crumbled under its own weight.

The European model—emerging from cross-analysis of YouGov, Coop, and GFI Europe data—follows a different logic: gradual integration. The fact that 59.3% of Italian households buy vegan products while declared vegans remain below 3% is telling. The winning strategy isn’t conversion, it’s inclusion. Make alternatives accessible, not ideological.

The core difference between the two markets lies in their target audience. The US aimed to win over meat lovers through perfect imitation, while Europe targeted pragmatic flexitarians looking for variety, not substitution. This strategic divergence explains why Italy’s plant-based deli segment (+20.9%, Coop 2025) appears more stable and less vulnerable to cultural backlashes.

As we outlined in our 2024 Annual Report, these trends confirm the structural resilience of Italy’s vegan market. Our forthcoming Plant-Based Market Analysis Report 2025 will delve deeper into these dynamics, comparing European and American strategies and exploring their implications for industry players.

The lesson for companies is crystal clear: the vegan market grows when it’s positioned as an addition to the food landscape, not an ideological alternative to tradition.