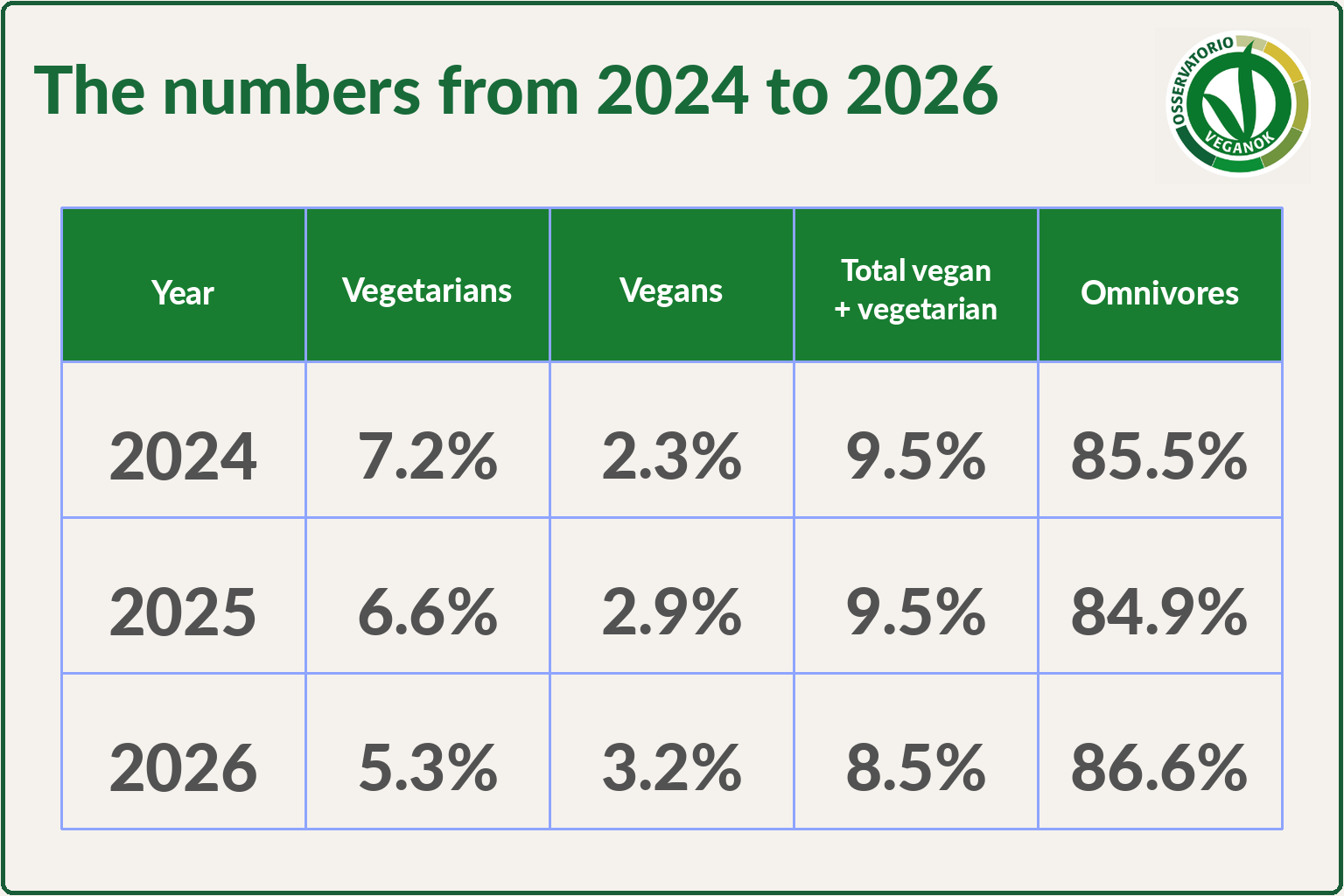

In 2026, vegetarians and vegans make up 8.5% of the population. The combined figure is down from 2025, but the vegan share climbs to 3.2%, the highest reading in the entire Eurispes time series. Meanwhile, opposition to factory farming, fur, animal circuses and hunting keeps growing: a sign of a cultural shift that goes well beyond what ends up on the plate.

Every year, the Eurispes Report gets read mainly with one question in mind: how many vegetarians and vegans are there in Italy?

It is an important question, but on its own it no longer tells the full story. The way Italians relate to food, animals, health and supply chains is becoming more layered. The dietary number still matters, yet it needs to be read alongside other signals: sensitivity toward animal exploitation, the rise of “free-from” products, the spread of functional foods, the role of nutritional information, and the still very wide gap between intention and practice.

The Rapporto Italia Eurispes 2026 captures exactly this complexity. It does not describe an Italy turning vegetarian or vegan in a straight line. It describes something more interesting: a country where the total share of people identifying as vegetarian or vegan falls compared with the previous year, while the vegan share rises; a country still overwhelmingly omnivorous, yet increasingly opposed to practices that make animal exploitation visible; a country where many citizens look favorably on a more plant-based diet but worry they will not manage to stick to it.

Put another way: the change is real, but it does not move in a straight line.

The numbers from 2024 to 2026

To read the 2026 figure correctly, you have to start with the past three years.

The first data point to face honestly is this: in 2026 the combined share of vegetarians and vegans drops from 9.5% to 8.5%. So it would be wrong to tell a story of broad, undifferentiated growth for the “veg” community.

But inside that decline sits an important signal. What shrinks is mainly the vegetarian share, which goes from 6.6% to 5.3%, while the vegan share grows from 2.9% to 3.2%. Veganism reaches its highest point in the entire Eurispes series.

This shift is the heart of the matter. The overall figure contracts, yet the vegan choice is consolidating. Eurispes points out that, over recent years, a vegan share of around 2 to 3% can now be considered an established feature of the population. The long-range picture is even more telling: between 2014 and 2026, the share of vegans in Italy has multiplied fivefold, rising from 0.6% to 3.2%.

We are looking at a phenomenon that is stabilizing and consolidating over time, even within the yearly swings of the combined vegetarian-plus-vegan total.

Fewer vegetarians, more vegans: what does it actually mean?

The difference between vegetarianism and veganism matters. Vegetarianism cuts out meat and fish but can still include dairy, eggs, cheese and other animal-derived foods. Veganism excludes everything of animal origin and usually grows out of a broader outlook that takes in our relationship with animals, with consumption, with supply chains and with exploitation in all its forms.

The fact that the vegan share grows in 2026 while the vegetarian share falls can be read as a sign of sharper definition. Part of the population may be stepping back from partial or on-and-off dietary choices, while those who commit to veganism look like a more stable, more conscious segment.

This reading matters for companies too. It does not mean the market should speak only to people who call themselves vegan. It does mean there is now an established vegan base, more visible and more recognizable, with a much wider audience moving around it: curious people, health-minded shoppers, those who care about animals, those drawn to “free-from” products, or simply people looking for options that fit their values better.

Veganism, then, should not be read only as an identity percentage. It also works as a cultural indicator: a choice that is small in raw numbers but able to shape language, products, claims, supply chains and consumer expectations.

The real headline: rising rejection of animal exploitation

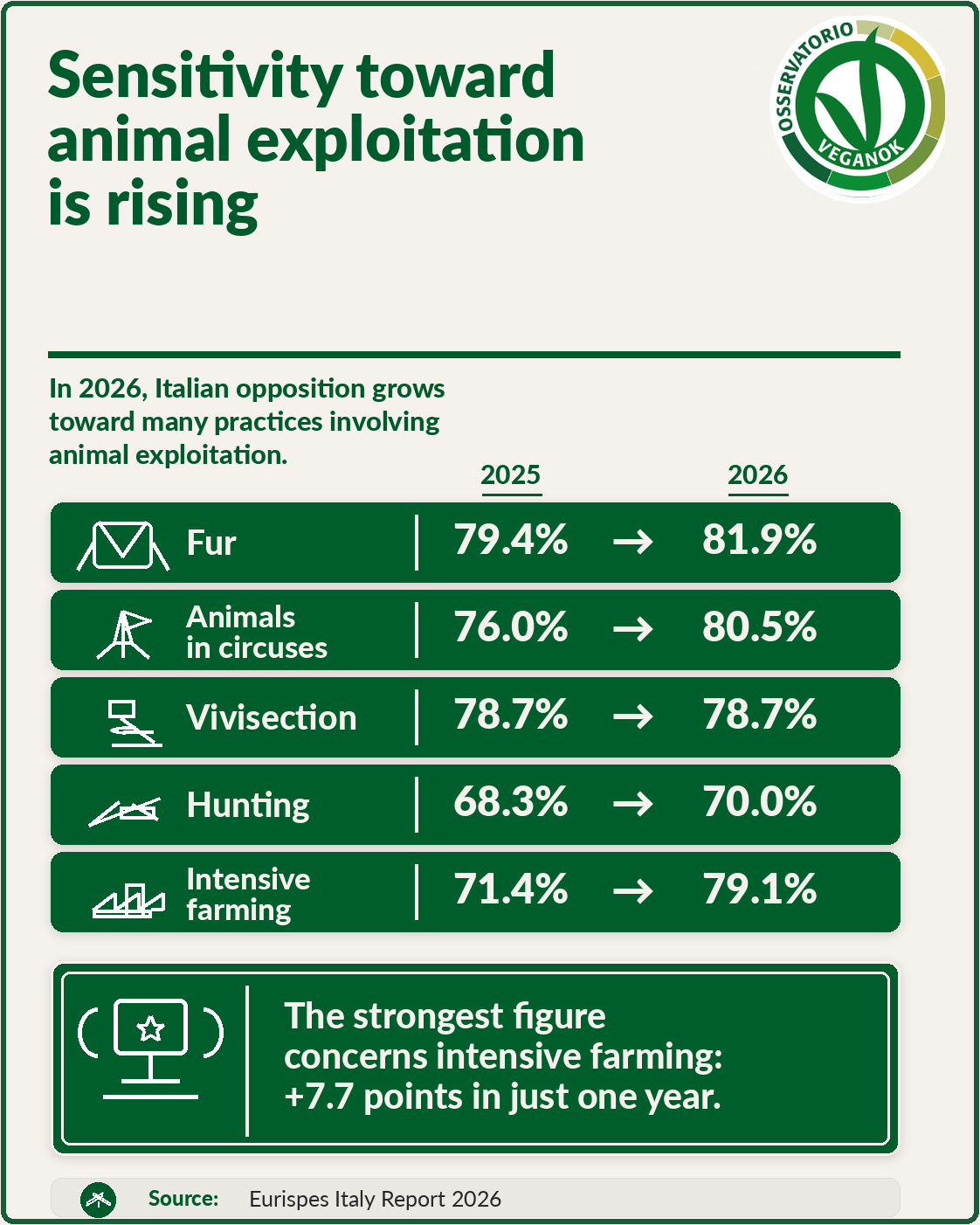

The strongest finding in the Eurispes 2026 Report, though, is about social attitudes toward animals.

81.9% of Italians say they are against the use of fur, up from 79.4% in 2025. 80.5% oppose the use of animals in circuses, compared with 76% the year before. 78.7% are against animal testing, broadly stable versus 2025. And 70% say they are against hunting, up from 68.3%.

The most significant shift, however, concerns factory farming: in 2026, 79.1% of Italians say they are opposed, against 71.4% in 2025. That is a jump of 7.7 percentage points in a single year.

Here the report says something important: most Italians still describe themselves as omnivores, yet they are less and less willing to accept the practices that make animal exploitation visible. Eating habits are not changing at the same speed as ethical sensitivity. The way people see things shifts first; behavior follows, more slowly.

We have watched this play out in other areas. What was treated as normal for decades starts to be questioned. Fur, animal circuses, animal testing, hunting and factory farming are no longer seen by a growing part of the population as neutral or inevitable. They turn into ethical, social and political issues.

This is why the Eurispes data should not be boiled down to the single question, “how many Italians are vegan?” The more interesting question becomes: how far is society’s moral threshold toward animals actually moving? In 2026, the answer is clear. It is moving a lot.

The 20.5% who want to change but fear they cannot

Alongside people who are already vegetarian or vegan, Eurispes captures another sizable group: 20.5% of Italians say they would be willing to switch to a vegetarian diet but worry they would not manage to keep it up.

It is one of the most important findings in the report, because it describes an audience that has not changed its diet yet is far from hostile to the idea. The opposite, in fact: they look at it with interest, maybe with sympathy, maybe with longing. The block is not ideological. It is practical.

How do you cook it? How do you shop for it? How do you replace your usual dishes? How do you juggle family, work, social life, deep-rooted habits, limited time and the fear of getting it wrong?

That is the crux. Between sensitivity and everyday change there is an enormous gap. And that gap is exactly where people need tools, recipes, guides, accessible information and gradual pathways.

In food-marketing terms, this group might be called “veg-curious” or “plant-curious”: people who are not yet vegetarian or vegan but are culturally open to a more plant-based way of eating. For an observatory tracking the vegan market, this is a strategic data point, because it shows that the potential of the dietary transition is not limited to those who have already changed. It also includes everyone who wants to and has no idea where to start.

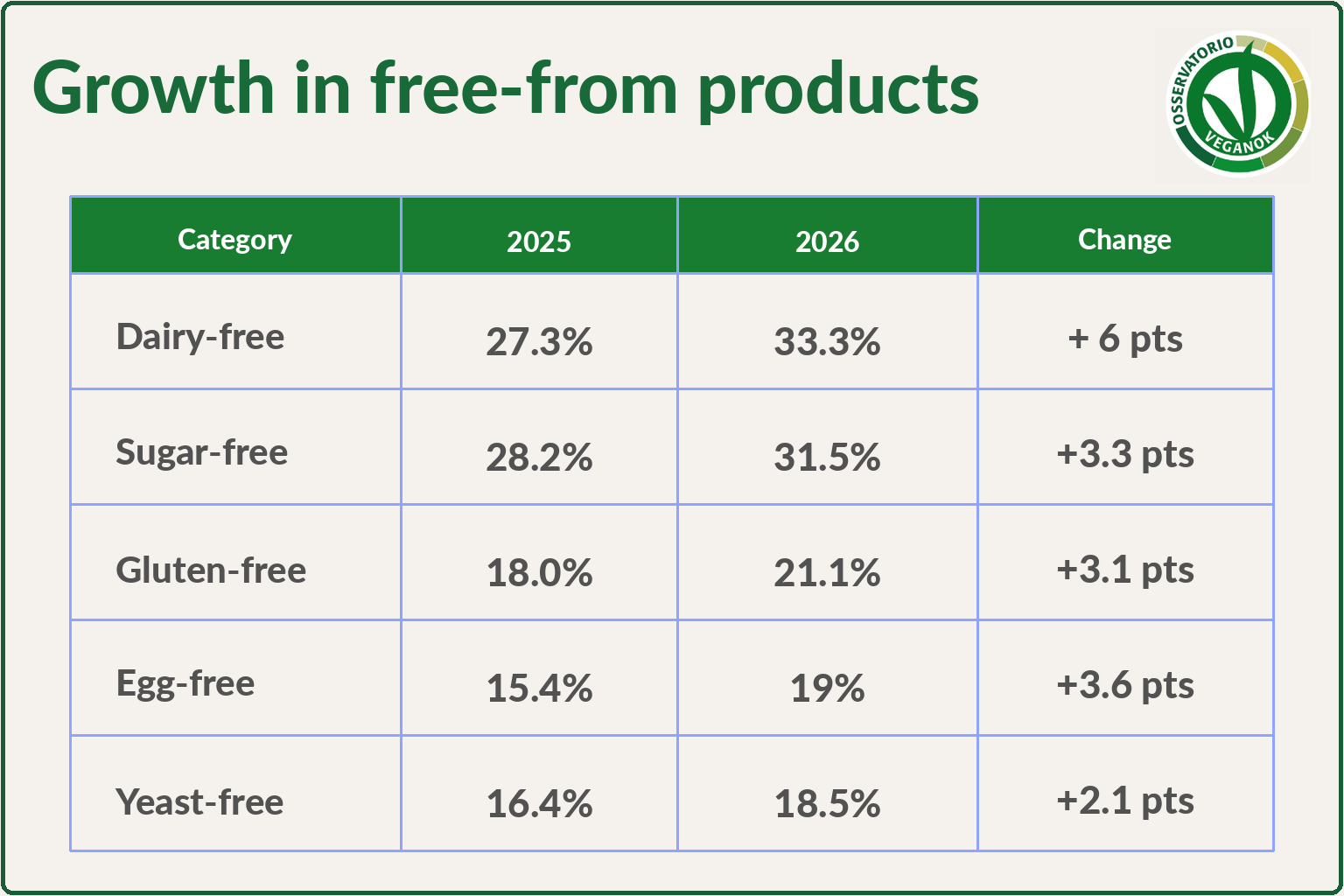

“Free-from” products are growing: it is not veganism, but it is a market signal

The Eurispes 2026 Report also shows growth in “free-from” products, meaning foods made without certain ingredients such as lactose, sugar, gluten, eggs or yeast.

The comparison with 2025 is clear.

A word of caution applies here too: “free-from” products are not automatically vegan. A lactose-free food can still contain animal ingredients; a gluten-free product has no necessary link to veganism; a sugar-free product may be chosen for dietary, health or calorie-control reasons.

But that is precisely what makes the data interesting. Italians are increasingly used to choosing food not only for taste, price or habit, but also for its composition, its ingredients, what it leaves out, its functional promises and how well it fits specific needs.

Eurispes also notes that many “free-from” products are bought by people with no certified allergies or intolerances. In other words, “free-from” has moved beyond the purely medical and into the territory of perceived wellbeing, lightness, prevention and personalized eating.

For the vegan market, this matters. Not because “free-from” equals vegan, but because it reveals a consumer who is more and more willing to read labels, question ingredients and look for alternatives. In that landscape, vegan certification can become a tool for clarity: not a vague claim, but a guarantee you can actually read inside an increasingly fragmented market.

The “egg-free” case: a signal for bakery, desserts and gelato

Among the data on “free-from” products, the egg-free figure deserves particular attention. In 2025, egg-free foods were bought by 15.4% of Italians; in 2026 the share rises to 19%.

It does not mean 19% of Italians are looking for vegan products. That would be a stretch. But it does mean interest in egg-free formulations is growing significantly.

It is a useful signal for plenty of sectors: baked goods, biscuits, desserts, gelato, pastry, and sweet and savory mixes. Eggs are one of the most widely used ingredients in the food industry, and replacing them is not only an ethical question. It can also answer needs around allergens, perceived lightness, inclusivity, shelf life, formulation innovation and simpler recipes.

For companies, this figure shows that vegan can speak to audiences well beyond the vegan community alone. A well-formulated, clearly communicated egg-free product can reach consumers with very different motivations: ethical, health-driven, functional or simply practical.

Health, protein, supplements: the consumer wants control

Another interesting part of the report covers functional foods, supplements and products seen as healthy or performance-oriented.

In 2026, 68.3% of Italians say they buy mixes of nuts and seeds. 62.1% use dietary supplements. 57% buy high-protein foods such as bars, yogurt, spreads, desserts and drinks. 49.5% consume probiotics and prebiotics, while 48.4% buy seeds like flax, sunflower, hemp and similar.

These numbers point to a consumer who cares a great deal about wellbeing, performance, nutrition and being in control of what they eat. Protein in particular has become an enormously powerful commercial language: it now shows up on snacks, yogurts, drinks, desserts and spreads that, only a few years ago, would never have been talked about in those terms.

But here too the picture is not clean. Alongside the pursuit of wellbeing, Eurispes records a very high intake of packaged and ultra-processed foods, bought by 62.6% of Italians. Another 64.4% also drink fizzy beverages, energy drinks and industrial fruit juices.

So today’s consumer is pulled in two directions: chasing health, protein, seeds, supplements and functional foods, while still living inside a food system that is industrial, fast, convenient and often ultra-processed.

That contradiction is especially sharp among young people. Between the ages of 18 and 24, 72.9% buy packaged and ultra-processed foods and 75.7% drink fizzy beverages, energy drinks and industrial fruit juices.

This is not about moralizing a generation. It is about reading the context: younger people are often more open to new ways of eating, but also more exposed to trends, quick-fix promises, industrial products and social-media messaging. And that is exactly where food information becomes decisive.

The problem is not only what we eat, but who we learn it from

The Eurispes 2026 Report also introduces an important data point on the sources Italians rely on to guide their food choices.

Nearly 4 in 10 Italians, 36.6%, say they turn to qualified professionals or scientifically reliable sources: doctors, nutritionists, naturopaths, medical journals or scientific websites.

At the same time, a portion of the population leans on less specialized sources: friends and family, social media, fitness influencers, personal trainers, forums, blogs, and non-medical books or magazines.

This matters because food today carries so many meanings: health, ethics, identity, environment, weight loss, performance, wellbeing, belonging. In a space that crowded with messages, the question is not only what Italians eat, but what tools they have to find their way.

That is why food information carries a growing responsibility. Talking about veganism, “free-from” products, protein, supplements or plant-based alternatives calls for clarity, verifiable sources and the ability to explain things well. Slogans are not what people need. Tools are.

What Eurispes 2026 really tells us

The Eurispes 2026 Report does not hand us a simple narrative. And that is exactly what makes it interesting.

It tells us the combined vegetarian-plus-vegan total falls, yet vegans grow and hit the highest reading in the historical series. It tells us most Italians remain omnivorous, yet rejection of animal exploitation keeps widening. It tells us there is a 20.5% who would welcome a vegetarian diet but are held back by the fear of not being able to keep it up. It tells us “free-from” products, functional foods, supplements and high-protein items are all on the rise. And it tells us that, in the middle of all this pursuit of wellbeing, ultra-processed foods, industrial drinks and not-always-reliable sources of information remain very common.

For the VEGANOK Observatory, the point is this: veganism cannot be measured simply by counting how many people call themselves vegan in a survey. That number stays essential, and in 2026 it grows. But around that number sits a wider cultural ecosystem: people starting to ask questions about animals, supply chains, ingredients, health, alternatives and the consistency between their values and their consumption.

The change is not linear. It is made of steps forward, swings, contradictions and new questions. But those very questions show where the market is heading.

In 2026, Italy does not suddenly turn vegan. It does, however, become more sensitive to animal exploitation, more used to looking for alternatives, more attentive to ingredients, and more in need of reliable tools to turn interest into everyday choices.

And it is in that space, between sensitivity and practice, that a big part of the future of plant-based food will be decided.